Cryptocurrency. Unless you’ve been hiding under a rock, you’d have surely been hearing this word at least once in a day!

Even though we all tend to have a vague “idea” as to what cryptocurrency is, most of us might not be paying any attention to the underlying technology. The fundamental technology that most cryptocurrencies and other emerging platforms rely on is – Blockchain.

Before we could go any further and dive deeper into the cryptocurrency ecosystem, let’s reverse-engineer to first understand the technology on which it’s built and then its applications.

Blockchain – What is it?

In its simplest form, a blockchain is a chain of blocks containing specific information or data grouped in a large network of linked computers in a secure and genuine mechanism.

In other words, every time we use the internet, we log into various applications and services, do banking online, exchange private data, browse, shop, and so on. Our governments, our economies, our societies run their core functions on the internet. All these activities produce data. By data, I mean about 2.5 quintillion bytes of data every single day.

Imagine blockchain as a historical fabric underneath, recording everything that is happening (transaction), exactly as it occurs in the above scenarios. Like an entirely new way of documenting data on the internet. All the recorded information is packed into several encrypted data blocks, and these link to form a chain with other blocks of similar information.

Once data is recorded in a block, it cannot be tampered with or altered without changing every block that came after it. The blocks are then distributed across the worldwide network. This makes it impossible for an intruder or a “hacker” to tamper with the data without going unnoticed by everyone else in the network.

Sounds like we have a solution to all our security concerns?

What is the problem blockchain is trying to solve?

Not all businesses or applications necessarily need blockchain to function efficiently and with integrity in the real world. Blockchain is ideal and works best for transactional systems. What do I mean by a transactional system then?

Let’s imagine a simple scenario.

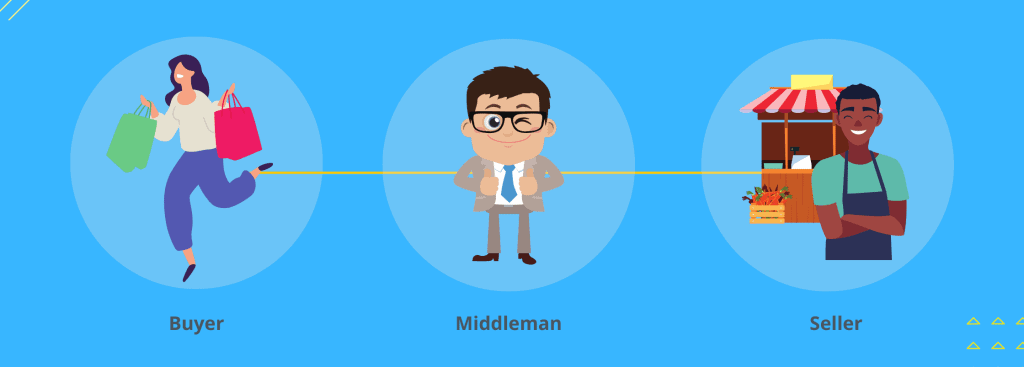

There’s a seller and a buyer. Both parties needed for a transaction to happen are present here and go ahead with the deal. So where is the need for a middleman in this? They can simply be cut out of the scene, right?

No.

Major industries like payments or securities clearing for instance have evolved through these middlemen. For example, a payment needs a business -> a customer and a bank in between. But why do we need these intermediaries like banks? Because they establish trust where there isn’t any other proven way of doing it. They establish ownership of the seller, that the seller has the right to sell what’s being sold. They check and approve that the history of transactions is clean. They also certify a buyer’s ability, that they have the money to buy what’s being sold.

When you don’t know the person on the other side of the transaction, (say the buyer doesn’t know the seller or the other way) intermediaries know and trust each other and enable the transaction. They document this transaction in their ledger and the parties completely trust the intermediary and the entry of the transaction in their ledger to be untampered with. The intermediaries’ business is based on this trust and they would only lose if they breach the trust. If it is all so clean, then where’s the real problem?

Like in all good stories, some intermediaries could go rogue and both the parties become vulnerable. Even though trust is the greatest concern, having intermediaries to facilitate transactions also involves huge costs, complexities, and high chances of error. These are some of the perceived risks involved in safeguarding the integrity of a transaction.

Trust is in the proof

Referring to our example above, which has a customer that purchases goods from a business, and the middleman bank, both parties here should trust the bank to intermediate this transaction and transfer the money. Apart from all the privacy concerns that might arise, the bank can suspend or reverse this transaction for any technical or feasibility reasons.

And that’s the advent of Blockchain – A technology, disrupting the entire ecology of intermediaries.

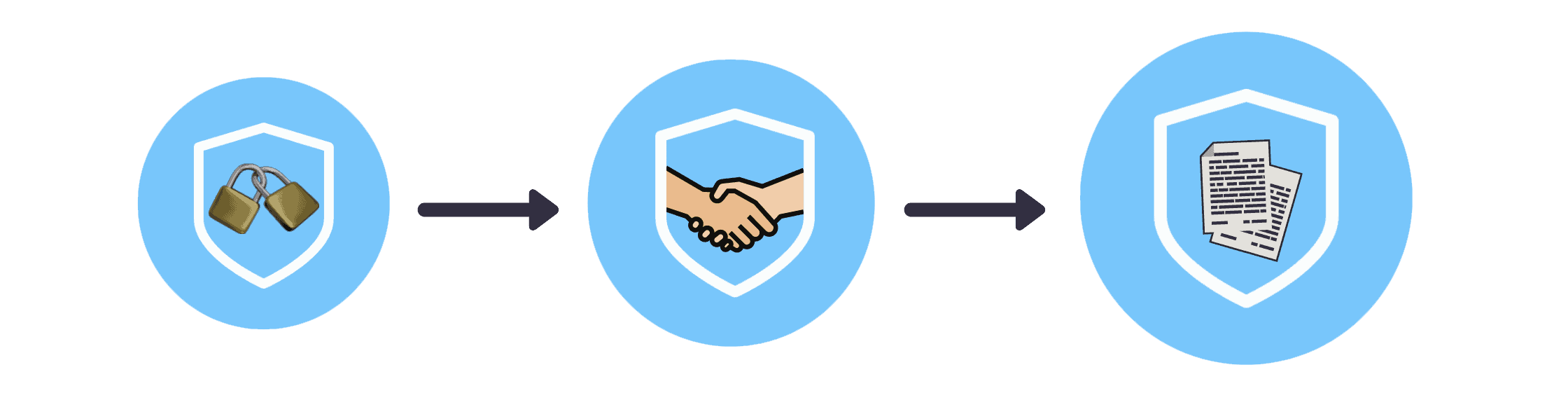

Werbach (2018) explains that there are three trustable elements in any transaction, including the counterparty, the intermediary, and the dispute resolution mechanism. blockchain tries to replace all three with software codes.

People or the counterparties are represented through arbitrary digital keys, which eliminate the contextual factors that humans use to evaluate trustworthiness. The transaction platform or the intermediary is represented by a network of distributed machines operated by unknown participants who are in it purely for the money. And dispute resolution occurs through “Smart Contracts” executing predefined algorithms. What makes a transaction valid are the cryptographic proofs that the other party can verify mathematically.

Businesses as we all know, never operate in isolation. They work together with other businesses, governments, banks, and many other types of organizations. This happens within a market system and significant wealth is generated across this network by the flow of goods and services. So, these business networks are interconnected by a lot of intermediaries.

This is where Blockchain comes into play. A distributed ledger relies on a large network of computers that encodes a transaction of digital assets between two peers without a centralized intermediary (or the middleman). The secure ledger provides an inviolable record, with an incorruptible history of transactions, and available to all the parties.

With this level of transparency, there is no need for a third party to vouch!

Blockchain is a proof of ownership, proof of history, and proof of ability in a non-centralized encrypted form, everything an intermediary would have been, the only difference being it’s not a human but a software code in the case of blockchain.

How do we achieve all this? – The core principles and functioning of a blockchain

The value of blockchain technology comes from the distributed security of the system. And so there a few key pillars to sustain the blockchain ecosystem.

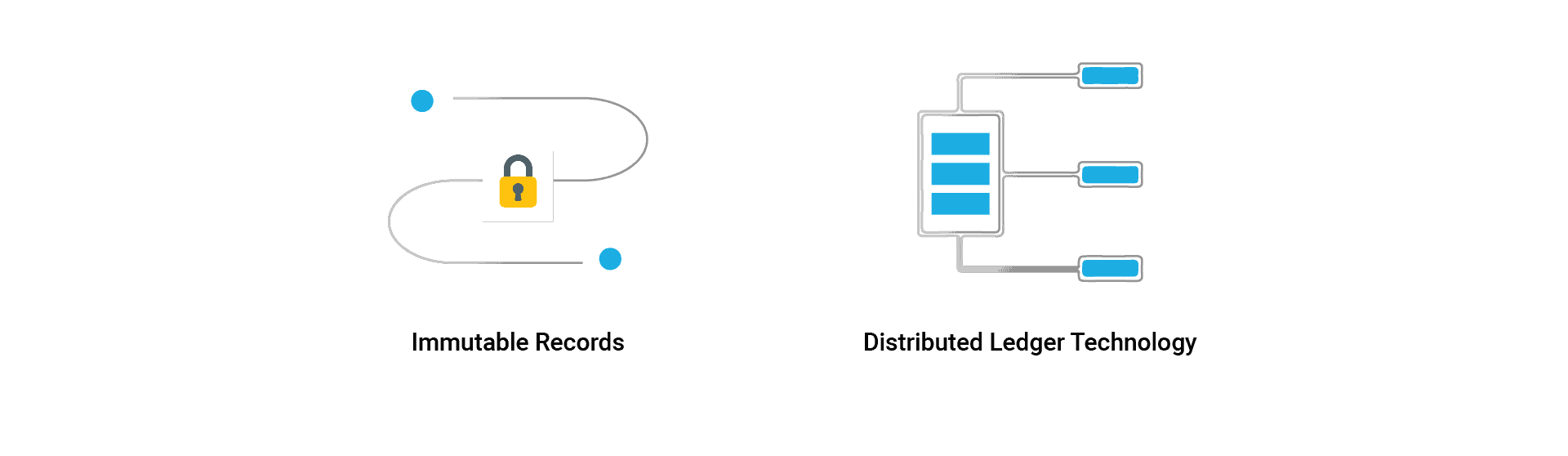

- A ledger can be appended with a piece of new information, but the previous information, stored in blocks cannot be edited or deleted. So, the ledgers are immutable

- The content of the newly added block is linked to each block before it using cryptographic hash or simply cryptography. This ensures that any change in the contents of the previous block in the chain would invalidate the data in all the blocks after it

- Blockchain data is distributed among all the users. Each user has a copy of the transactions and hashed blocks. They spread the information of any new transaction to the entire network. So they are a peer-to-peer (P2P) network that does not need any internal or external trust authority

- A large number of computers are connected to the network, bringing down the ability of an attacker to maliciously add transactions to the network. This is the principle of consensus. All the participants adding to blockchain must compete to solve a mathematical proof using either the Proof of Work and Proof of Stake method. Solving the problem is known as mining, and ‘miners’ are usually rewarded for their work in cryptocurrency. The results are shared with all the computers on the network. Each computer or node connected to this network must agree to the solution, arriving at a consensus

- No single entity can take control of the information on blockchain making it decentralized

- The network relies on agreement by multiple entities, so it is trustless

- Transactions recorded in the chain can be publicly published and verified such that anyone can view the contents of the blockchain and verify that the recorded transactions took place. Thus blockchains can be made public

A blockchain transaction

Let’s build a flow of a transaction in a blockchain

- Person A requests a transaction

- This requested transaction is broadcast to a peer-to-peer network consisting of a large network of computers or nodes

- The nodes validate the transaction and the user’s identity using algorithms

- Once all the nodes come to a consensus, the transaction is verified. The transaction could be of any nature, involving cryptocurrency, or other digital tokens, records, or other information

- The verified transaction is combined with other transactions to create a new block of data for the ledger

- The new block is added to the existing blockchain permanently and it is unchangeable

This completes a single transaction.

A transaction must go through several fundamental, critical, and decisive steps before it can be added to the blockchain. We’ve seen an outline of the multi-step process involved in a blockchain transaction. We’ll learn more about cryptographic keys and how they help in the authentication of the user, authorization via proof of work, mining and its significance, proof of stake protocols, and the more recent adoptions in our upcoming blogs.

What value can blockchain add to your business?

Blockchain technology has a lot to offer and as with any new technology, use cases, applications and adoption will expand as businesses begin to think intuitively and come up with creative solutions to integrate it into their processes.

While there’s still time for companies to send out invoices with crypto payment options, blockchain has started reshaping industries in the financial sector, accounting, healthcare, and insurance.

Reasons businesses should consider blockchain

- Security – We think digital, we think security. And business data and transactions are even more critical, sensitive, and are highly vulnerable to being tampered with. With blockchain decentralized systems, information is stored with an entire network making it impossible for an intruder to breach. Also, advanced cryptographic techniques used to encrypt information adds the silver shield to your data.

- No intermediaries All along this article we’ve seen how having an intermediary can give rise to the problem of trust. Blockchain is a trustless network and runs on cryptographic proof allowing two willing parties to directly transact with each other.

- Smart Contracts – Smart contracts are self-verifying, self-enforcing contracts stored within a blockchain ledger. The contract is once recorded, cannot be manipulated. These smart contracts offer small businesses a great level of protection which is otherwise an exorbitant investment for these businesses. Some examples of smart contracts are commercial leases, agreements, insurance policies, clinical data, recording real estate property ownership, and more.

This McKinsey&Company report assesses the strategic value of blockchain for companies in terms of cost and disintermediation as well as the creation of new business models.

In our following readings, we’ll see how Blockchain is “the” technology that’s going to impact most businesses in the next five years. And why you cannot afford to ignore this powerful technology.

Bitcoin is not blockchain. It is an application of blockchain technology

Have you heard of Bitcoin or Ethereum? Of course, you have! Well, blockchain is the underlying technology Bitcoin is built on.

What is Bitcoin?

Bitcoin is a currency, a digital currency that you can buy, sell and exchange directly with a counterpart without an intermediary like a bank. However, Bitcoin’s creator Satoshi Nakamoto describes Bitcoin as a “Peer-to-peer electronic cash system that does not rely on trust.”

Since we’ve mentioned Bitcoin as an application or digital currency developed under the principles of blockchain, every Bitcoin transaction that’s ever been made exists on a public ledger, that is irreversible or inimitable. And as blockchain provides decentralization, Bitcoins are decentralized in nature owing to which they do not have any backing central issuing authority like a bank or Government.

A Bitcoin blockchain

Multiple Bitcoin holders form the Peer-to-Peer network of the Bitcoin blockchain and ideally, Bitcoin transactions are messages like an email, which are digitally signed using cryptography and shared with the entire Bitcoin network for verification. All the transactions are public and can be viewed in the ledger. Backtracking all these transactions will lead to the first Bitcoin transaction.

We’ll learn more about how a Bitcoin transaction works in detailed blogs later.

Coins versus Tokens

We have been familiar with Bitcoin as a cryptocurrency for a long period. Following this, other types of coins came into existence as an alternative to Bitcoin, collectively known as altcoins. Even today, newer cryptocurrencies are being invented to support various blockchain applications. Depending on the application and its functionality, tokens are grouped into 5 major categories:

- Utility tokens – These tokens are launched by a company to provide its users with a mechanism to pay for a new product or service developed by the company, developed on blockchain technology.

- Currency tokens – It is like a real currency used for payments against purchases. Bitcoin is a currency token, a digital currency that can be used to make online/offline purchases, traded for other cryptocurrencies, or even transferred to other users.

- Security/ Equity tokens – Also known as equity tokens, security tokens work like traditional securities. They act like a share or stock of a company given to a buyer. The value of these tokens is volatile and is subject to the project’s performance, just like stocks.

- Reward tokens – These are special tokens, given as rewards to someone as a mark of appreciation. The value of these tokens may differ from the other tokens.

- Asset tokens or Non-Fungible tokens (NFT’s) – An NFT is a digital asset that represents real-world objects like art, music, in-game items, and videos. They are bought and sold online, frequently with cryptocurrency, and they are generally encoded with the same underlying software as many cryptos.

Regular bank currency and cryptocurrencies are “fungible,” that is, they can be traded or exchanged for one another. They’re also equal in value—one dollar is always worth another dollar; one Bitcoin is always equal to another Bitcoin. Crypto’s fungibility makes it a trusted means of conducting transactions on blockchain.

NFTs on the other hand is different. Each token has a digital signature that makes it impossible for NFTs to be exchanged for or equal to one another making them non-fungible.

How to use Bitcoins?

In recent times, Bitcoin is perceived as an alternative investment, helping investors to diversify their portfolios apart from stocks and other funds. Although the number of vendors accepting cryptocurrencies is still limited, you can use Bitcoin to make purchases of goods and services.

That being said, PayPal made a major announcement around cryptocurrencies this year. They announced the launch of a new service enabling their customers to buy, hold and sell cryptocurrency directly from their PayPal account, and signaled its plans to significantly increase cryptocurrency’s utility by making it available as a funding source for purchases at its 26 million merchants worldwide.

We’ll discuss more on how you can buy Bitcoins and other cryptocurrencies, their financial implications, and Bitcoins as a source of investment in our upcoming blogs.

All that you’ve read above, explains theoretically what a blockchain is and how it’s a technology we must adopt for the better. But it’s hard to imagine how this technology is put to use in real life, who are the users of this technology, and who benefit from it. Don’t worry! This article is just a high-level overview of blockchain. So the next time you come across the term anywhere, you are not guessing what it is.

In our upcoming blogs

In our forthcoming series, we’ll dive deeper into every aspect of blockchain technology, its stakeholders, and how businesses can leverage this technology to its advantage.